Check out the database: “Quantum technology providers”

With more than 200 active companies, the field of quantum computing is continuously growing, supported by the large infusion of capital coming from governmental projects, the quest of investors for promising technologies and the desire of companies from different industries to stay up to date with the latest technology.

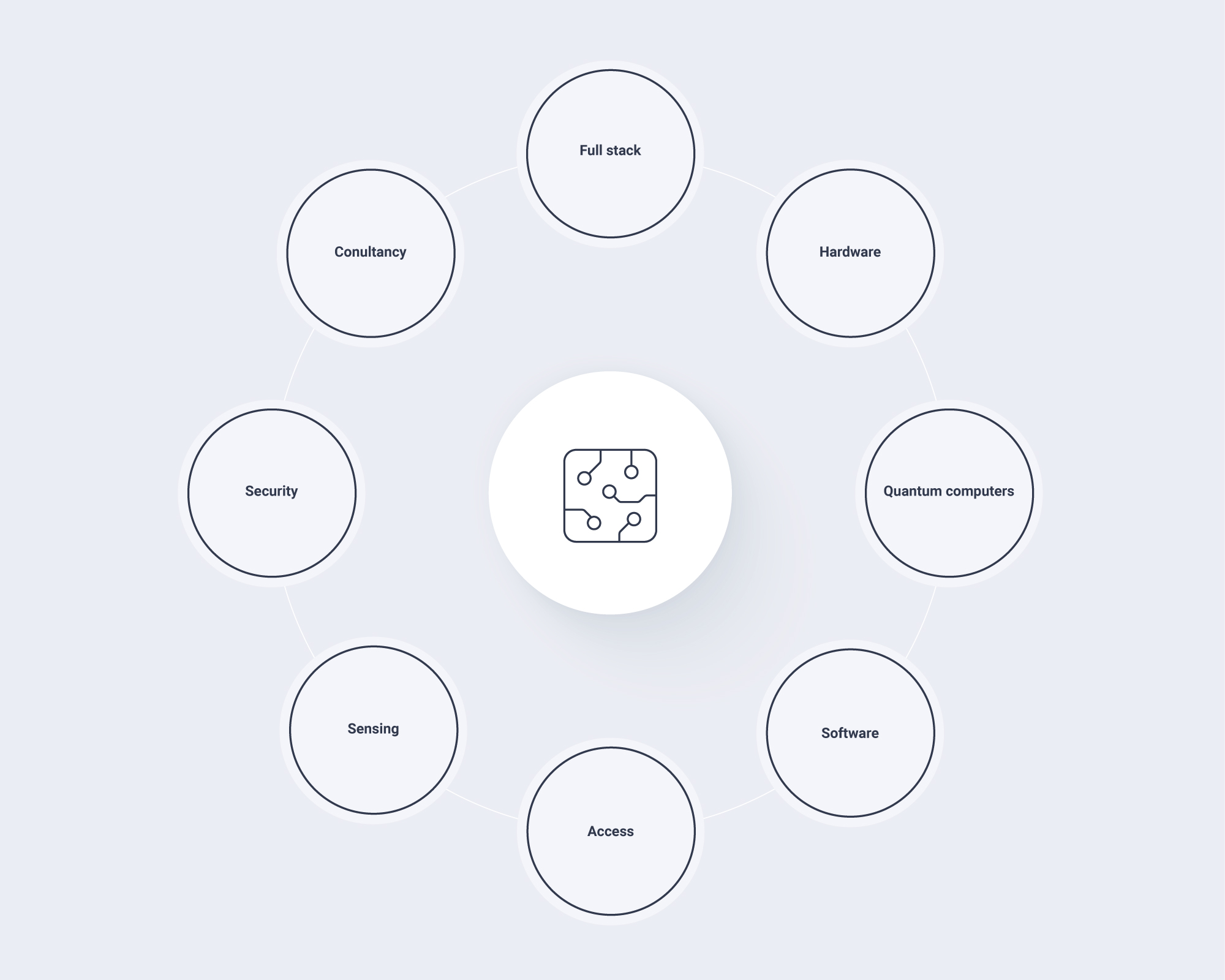

The main providers of devices and services in this sector can be divided into several categories:

Full-stack providers cover the development, production, and scaling-up of quantum devices, as well as the software, interface, and applications development.

The main companies in this sector are IBM, Google, Rigetti, Alibaba, Microsoft, D-Wave, and Xanadu. Other companies such as IQM Finland or Oxford Ionics are still in an emerging phase, showing promise and potential but still having to catch up with the industry leaders.

Quantum computer providers are focused only on producing the devices and scaling them up. Usually, they partner up with other companies and research centers for software and applications development.

Main companies: Alice&Bob (superconducting technology), Anyon Systems (superconducting), Atom Computing (individual atoms), Equal1Labs (silicon-based), IonQ (trapped ion), NextGenQ (trapped ion), Origin Quantum Computing (superconducting and quantum dot), Oxford Quantum Circuits, Pasqual, PsiQuantum (photonic), Quantum Factory (trapped ion), QuEra Computing (cold atoms), Silicon Quantum Computing, Universal Quantum.

Hardware components providers concentrate on individual elements that are necessary for quantum technology to function, such as quantum repeaters (to speed up the photons in the future quantum internet), solutions for qubit storage, refrigeration systems, photon detectors, test and measurement instruments, etc. Some of these companies develop a wide range of services and products and, with quantum-dedicated components being only a part of them.

Main companies: Intel (develops quantum chips), Archer Materials (carbon-based qubits), Braket Science (solutions to room-temperature qubit storage), Delft Circuits (quantum hardware), InfiniQ (quantum hardware that can operate at room temperature), Keysight Technologies (qubit control solutions and measurement instrumentation), Orca Computing (quantum memory), QuiX (light-based quantum processor), Universal Quantum Devices (electronic instrumentation products for quantum measurements).

Software companies: Current quantum devices are prone to errors and special developed software would be one approach to lower the number of these errors and diminish their impact. Software companies usually partner with full-stack and quantum computers providers to implement and test their programs and hopefully increase the stability of the devices.

Main companies: Nordic Quantum computing group (develops software for superconducting and photonic quantum devices), Opacity (produces Quiver, a software aimed to detect and suppress errors across quantum computations), Q-Lion (error-correcting software for trapped ion devices).

Quantum access companies facilitate access to this type of technology by building interfaces, simulators, or applications for different industries and purposes. These companies usually have a multidisciplinary team and expertise in quantum technology as well as in areas where quantum computations could be successfully implemented. Moreover, they have expertise in reframing problems and algorithms so that they match the current capabilities of quantum devices.

Main companies: ApexQubit (uses quantum computing for small molecules and peptides discovery), Automasky (develops simulators and quantum algorithms), Avanetix (develops quantum applications for transport and manufacturing industry), Cambridge Quantum Computing (provides software for different types of quantum devices, as well as quantum solutions for chemistry, machine learning, and security), Huawei (a cloud service platform for quantum simulation), M-Labs (control system for quantum information experiments), QbitLogic (quantum machine learning and quantum algorithms), Quacoon (using quantum algorithms to address optimization problems within the manufacturing industry), Speqtral (the first company that demonstrated the entanglement of photons in space), Spin Quantum Tech (development of quantum algorithms to speed up their artificial intelligence solutions).

Quantum sensing companies develop sensors that make use of quantum properties to perform measurements of physical bodies, with direct applications in areas that require extremely high precision. Even though quantum sensors such as magnetometers and atomic clocks have long been developed, this sector has recently registered rapid growth.

Main companies: Miraex, Muquans, Qnami, Raytheon

Quantum security companies are developing quantum-safe cryptographic systems that can be applied to various industries to protect their stored data and secure their communications.

Main companies: CryptaLabs (develops quantum random number generators that are very useful for the encryption process), InfiniQuant (solutions for securing metropolitan and satellite communications), Post-Quantum Solutions, Quintessence Labs, Quant LR.

Consultancy companies provide a link between the quantum technology developers and different industry sectors. Some of them help businesses assess whether their products and services could benefit from the potential advantages brought by quantum computers, while others help with software and algorithm adjustments, customized research on possible applications or technologies, etc.

Main companies: QuantumPhi (consultancy services related to quantum technologies and their application), Quantika, Phase Space Computing (educational tools for quantum information science), OneQuantum (start-up community with access to various resources), H-Bar Consultants (overview of key technologies and investment opportunities).

Market overview

Market overview

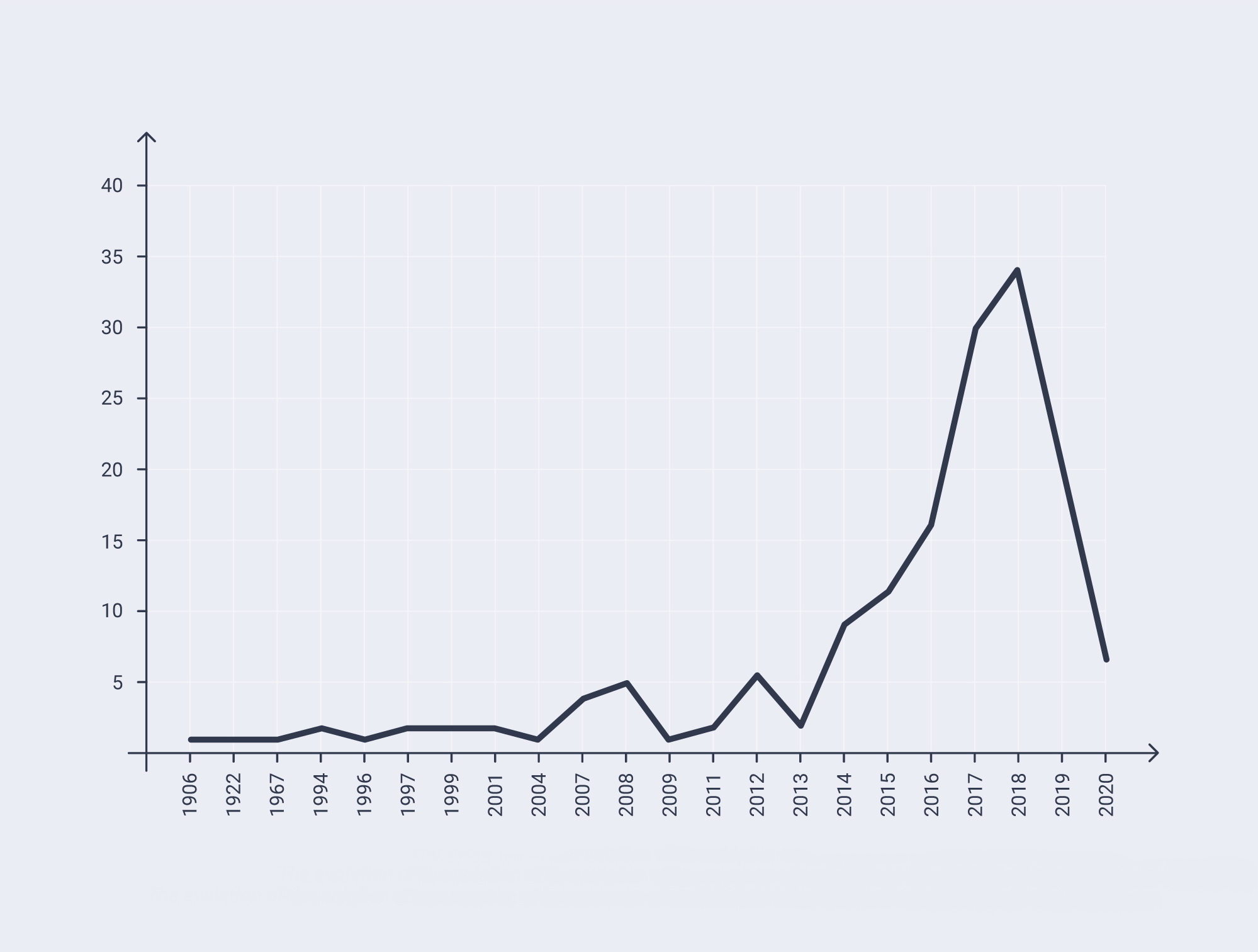

The number of companies in the quantum technology field registered a steep increase in the last couple of years, with a peak in 2018 (for already established companies, we considered the year when quantum projects were started). Many companies funded from 2017 onward are still working to develop their products and penetrate the market. However, many developments in the field depend on the actual improvements of quantum technologies.

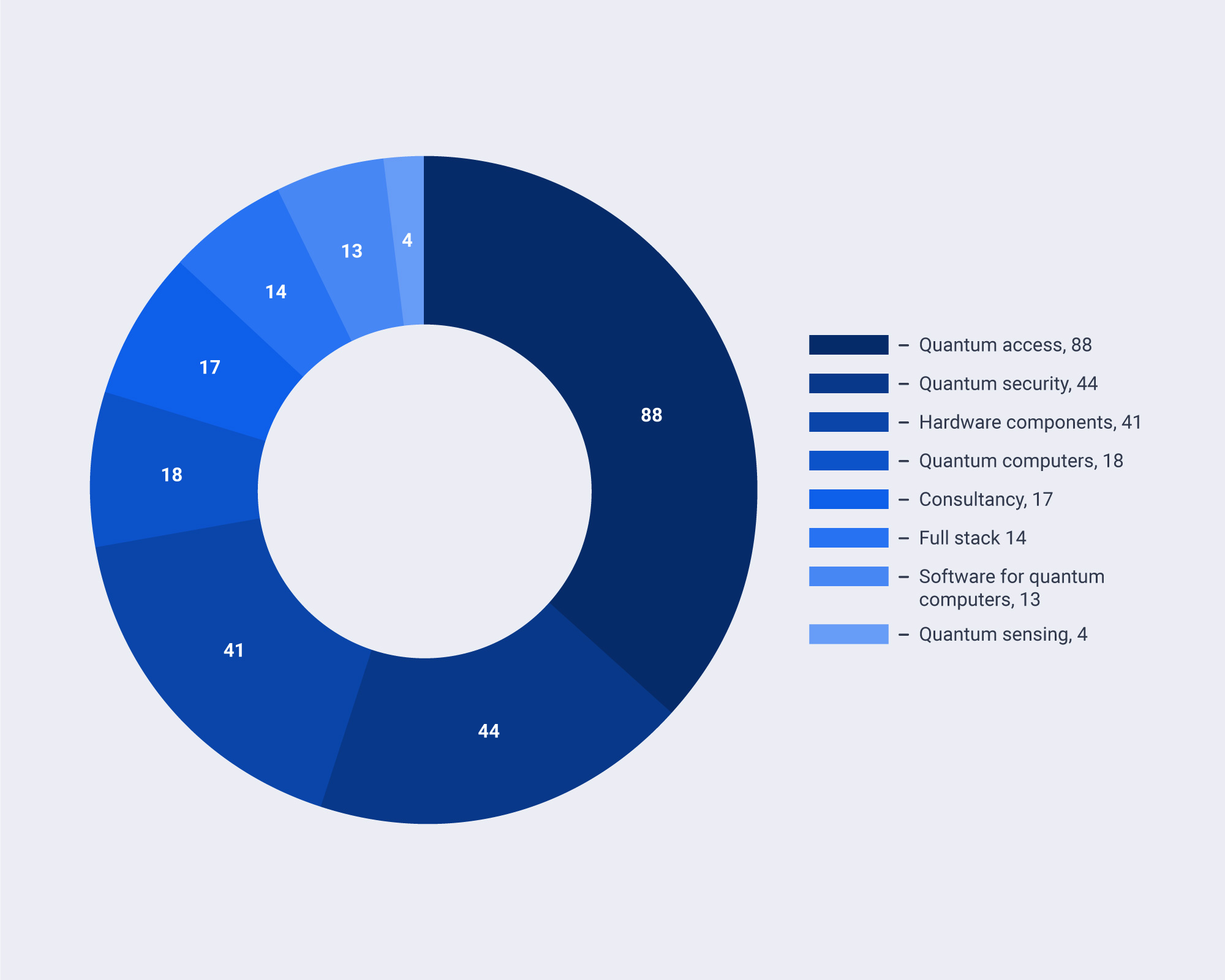

The majority of the 239 companies investigated provide services related to quantum access. This type of activity focuses mostly on know-how and field expertise and doesn’t require extensive physical resources, which could explain the high number of companies in this sector. Most of the quantum access services are not hardware-dependent, even though most quantum access providers have their preferred quantum technology providers and access their devices via the cloud. Other activities such as simulation development can be conducted on conventional devices.

The quantum threat is a prevailing concern in the media. As a consequence, many start-ups have focused their services on cryptography, providing quantum key distribution and secure solutions for communications. This makes this sector the second-most relevant in terms of the number of service providers. Moreover, this area also has the highest market potential. The number of companies dealing with problems that could be solved by quantum computers may be limited, but all institutions and businesses need to protect their data and communication processes.

The companies providing hardware components come third, most of them doing specific research on qubit technologies or refrigeration systems. Of the companies selected for investigation, only 7 percent build quantum computers, and 5 percent provide full stack services. The human, financial, and equipment requirements are relatively high in this sector. Therefore, the barrier to entry is higher and not attainable for the majority of startups. Most of companies in this category are either established public companies with large research and development budgets, or startups that have managed to attract significant investments.

The number of companies developing software for error-correction is relatively low, possibly because this type of activity is mostly conducted in university research centers or by full-stack providers. The output might be harder to commercialize and would have limited market coverage.

Since no real-world applications have been developed yet, the number of consulting companies is relatively low. Most of them provide market overviews or an evaluation of industry-specific problems that might be tackled through quantum computations.

As Sayonee Ray, Supertrends expert and post-doctoral fellow at the Center for Quantum Information and Control in New Mexico has stated, quantum sensing is a very promising field where significant advancements have already been made. However, the number of companies in this field remains low.

Major players

Major players

The field of quantum computing is currently dominated by several major players, including both public and private companies, that have managed to achieve significant results in the race towards quantum supremacy and advantage.

With a fleet of 28 quantum computers, most of them accessible via cloud, IBM leads the way in terms of achievements, accessibility, and involvement in the research. Through its IBM Q network, it brings together over 50 companies, academic institutions, start-ups, and research centers to accelerate the development in the field of quantum computing. The maximum number of qubits developed on their devices is 53; however, IBM achieved a quantum volume of 64 in August 2020 on a 27-qubit device.86 IBM also developed a supercomputer (IBM Summit) that was used to challenge Google’s claim of achieving quantum supremacy. Aiming to achieve 1,000 qubits by 2023,87 IBM already works with companies such as JP Morgan, Barclays, and Samsung to help them develop and implement quantum strategies.

After investing in superconducting technology, Google claimed in 2019 that that it had achieved quantum supremacy on a 54-qubit quantum computer. Currently, it focuses on quantum device and software development, aiming to accelerate AI applications. Besides quantum computing, Google’s main research areas are quantum simulations, quantum neural networks, qubit metrology, and quantum-assisted optimization. Volkswagen and Daimler are among their customers for this particular technology.

Microsoft built its first quantum computers on superconducting technology, but is currently experimenting with silicon spin qubits and topological qubits as well. It works in partnership with universities in Denmark, the Netherlands, the US, and Australia. It offers an open-source quantum development kit and access to quantum devices via Microsoft Azure.

After two generations of quantum processors, Intel has currently reached 49 superconducting qubits. The quantum chips are developed by Intel, but they are integrated into quantum computers by QuTech, a Dutch company. The software and applications are developed in collaboration with the University of Toronto and University of Chicago. Currently, Intel and its partners are experimenting with spin qubits, a promising technology that might surpass superconducting qubits in terms of stability and operating temperature.

With a long history in quantum computing research, Alibaba opened its first quantum center in 2015. In 2018, it launched its quantum computing cloud, providing access to a 11-qubit quantum processor. Currently, it uses the Alibaba Cloud Quantum Development Platform (AC-QDP) and Tai-Zhang, a classical simulator of quantum circuits, to design and test quantum algorithms.

D-Wave is the world’s first quantum computing company. Using annealing technology, it has already developed over 250 early quantum applications for industries such as chemistry, healthcare, automotive, transportation, and manufacturing. Defense contractor Lockheed Martin, D-Wave’s first customer, was one of the first companies to acquire its own quantum computer. It is important to keep in mind that quantum annealing is a different “dialect” of quantum computing and is not directly comparable to gate-based, general quantum computing.

Rigetti currently owns a 31-qubit superconducting device. Via its Quantum Cloud Services, it provides access to hybrid quantum-classical computation that supports ultra-low latency connectivity (the capacity to process very large amounts of data in a short timeframe, allowing for real-time access and fast reaction when data changes). Clients can access Rigetti’s resources through network APPIs. Since 2020, Rigetti has been the leader of a £10 million consortium that aims to accelerate the commercialization of quantum computing in the UK.

Building upon an extensive expertise in manufacturing, chemical development, aerospace, control systems, etc., Honeywell decided that it already has the technology and the required know-how to step into the quantum computing industry. While Honeywell focuses only on building trapped ion quantum devices, the company has partnered with Cambridge Quantum Computing for software and algorithm development.

In addition to a 11-qubit device that is already commercially available via Amazon Bracket, IonQ in October 2020 released a new 32-qubit device based on trapped ion technology, which theoretically has the potential to achieve a quantum volume of 4,000,000. Along with that, two more generations of quantum computers are under development, and IonQ aims to double the number of qubits every year. Together with Zapata Computing, the company is developing and implementing industry applications.

In September 2020, Xanadu brought the first photonic quantum computer to the cloud. The advertised advantage of this type of technology is that it can operate at room temperature and is easy scalable, making it a very good candidate for use in future FTQCs.

These companies collaborate with university centers and representatives of different industries, usually focusing on three main aspects: the technological development of the device, software and algorithm development, and testing possible applications.

Promising start-ups

Promising start-ups

As investments and governmental funds are flowing, new companies are constantly joining the quantum race. PsiQuantum, a Californian company established in 2016, raised US$215 million in 2020 and has secured US$508 million in overall funding to date. It aims to reach one million silicon photonic qubits “within a handful of years”.88

With several quantum devices located in Innsbruck, Austria, Alpine Quantum Technologies (AQT) employs trapped ion technology to develop quantum applications together with clients and partners.

Building upon the expertise of Professor Winfried Hensinger, director of the Sussex Centre for Quantum Technologies, and with the help of a multidisciplinary team, Universal Quantum, an UK-based company, has also set the bar high, aiming for one million trapped ion qubits.

Pasqal, a French start-up, claims to be on track to build a quantum simulator consisting of several hundred qubits by the end of 2020 and provide remote access to it in 2021. The company has also stated that it is working on assembling its first 200-qubit computer, and is already building a second one dedicated to their cloud computing service (available from the end of 2021). At the same time, Pasqal has partnered with Qubit Pharmaceuticals to define application classes related to computational drug design.

Having developed the first commercial qubits in the UK, Oxford Quantum Circuits has stated that it already has a complete functional quantum unit (hardware and software), which it claims is the most advanced and the only commercially available quantum computer in the UK.

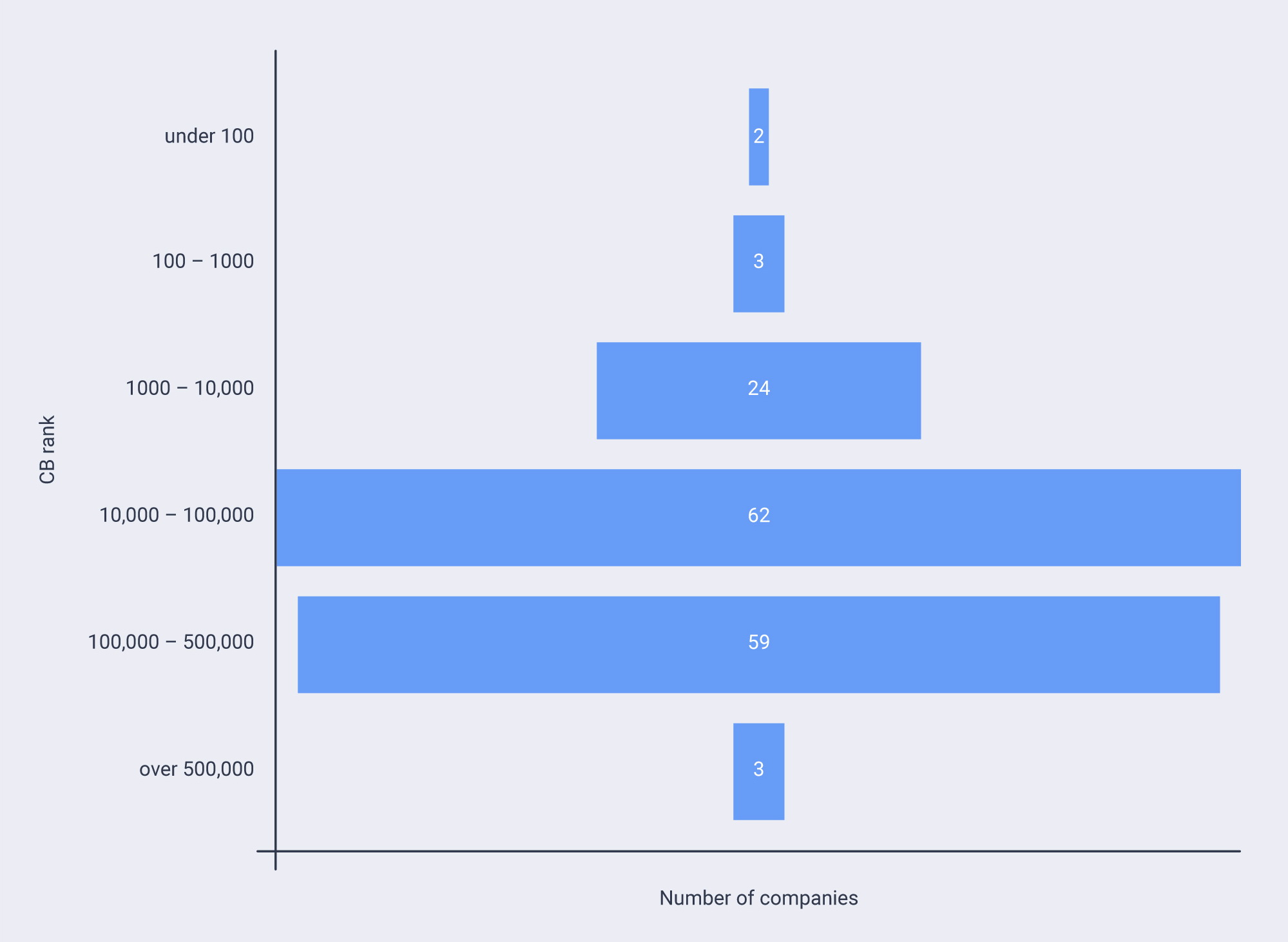

Out of the 239 quantum players that were investigated, 153 had a rank associated on Crunchbase. As a platform that aggregates business information about public and private companies, Crunchbase only ranks the top 100,000 companies in each industry, based on criteria such as the number of profile connections within the platform, community engagement, news, funding rounds, etc.

Apart from established companies such as Google, Alibaba, Intel, etc., which rank very high, the majority of quantum companies have a Crunchbase rank between 10,000 and 500,000, meaning that they are still in the incipient phase, building up their visibility and impact on the industry. Unlike recognized companies with large budgets and teams, these organizations can be targeted by anyone wanting to enter this field, either for future investments or for business partnerships.

Regional distribution

Regional distribution

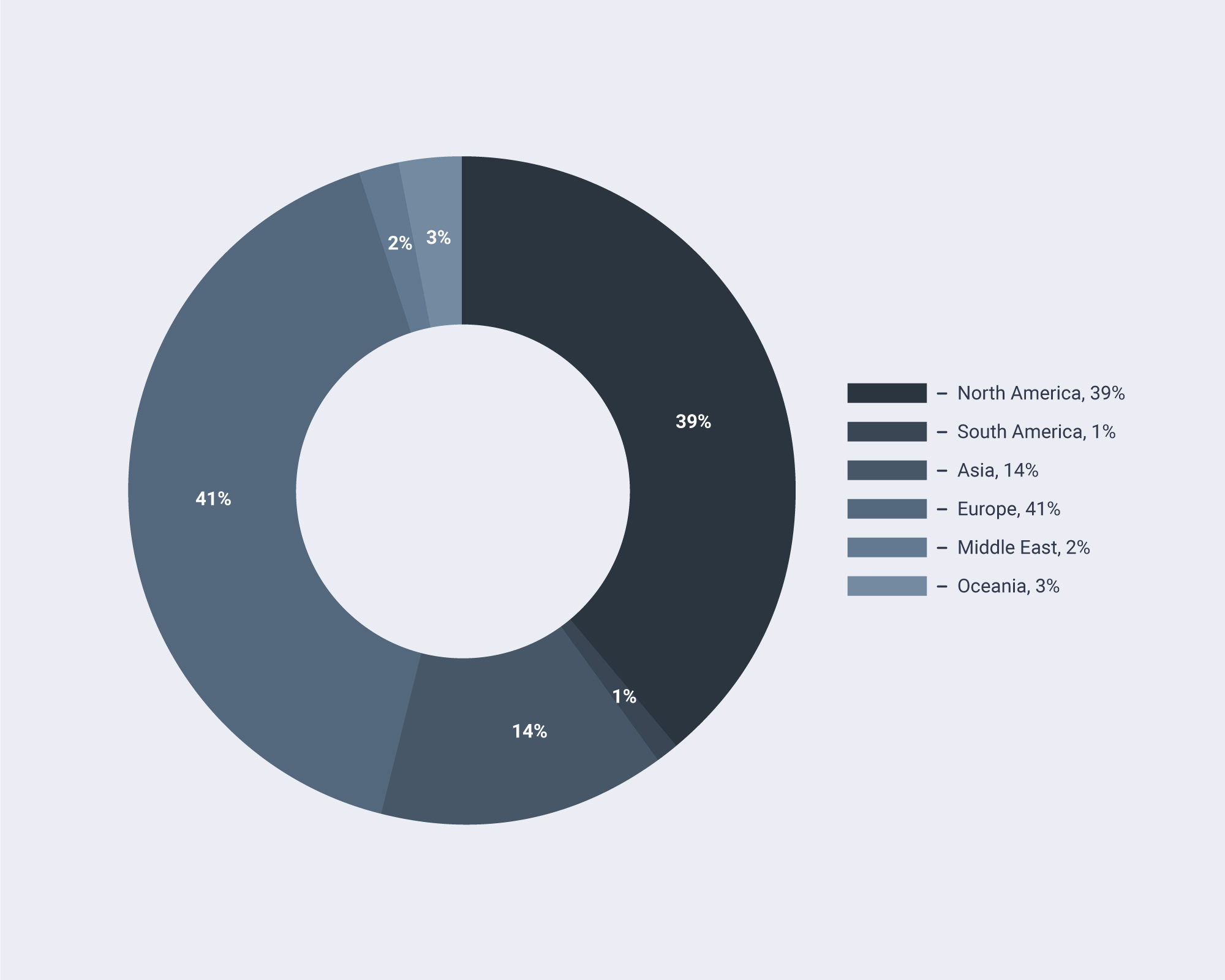

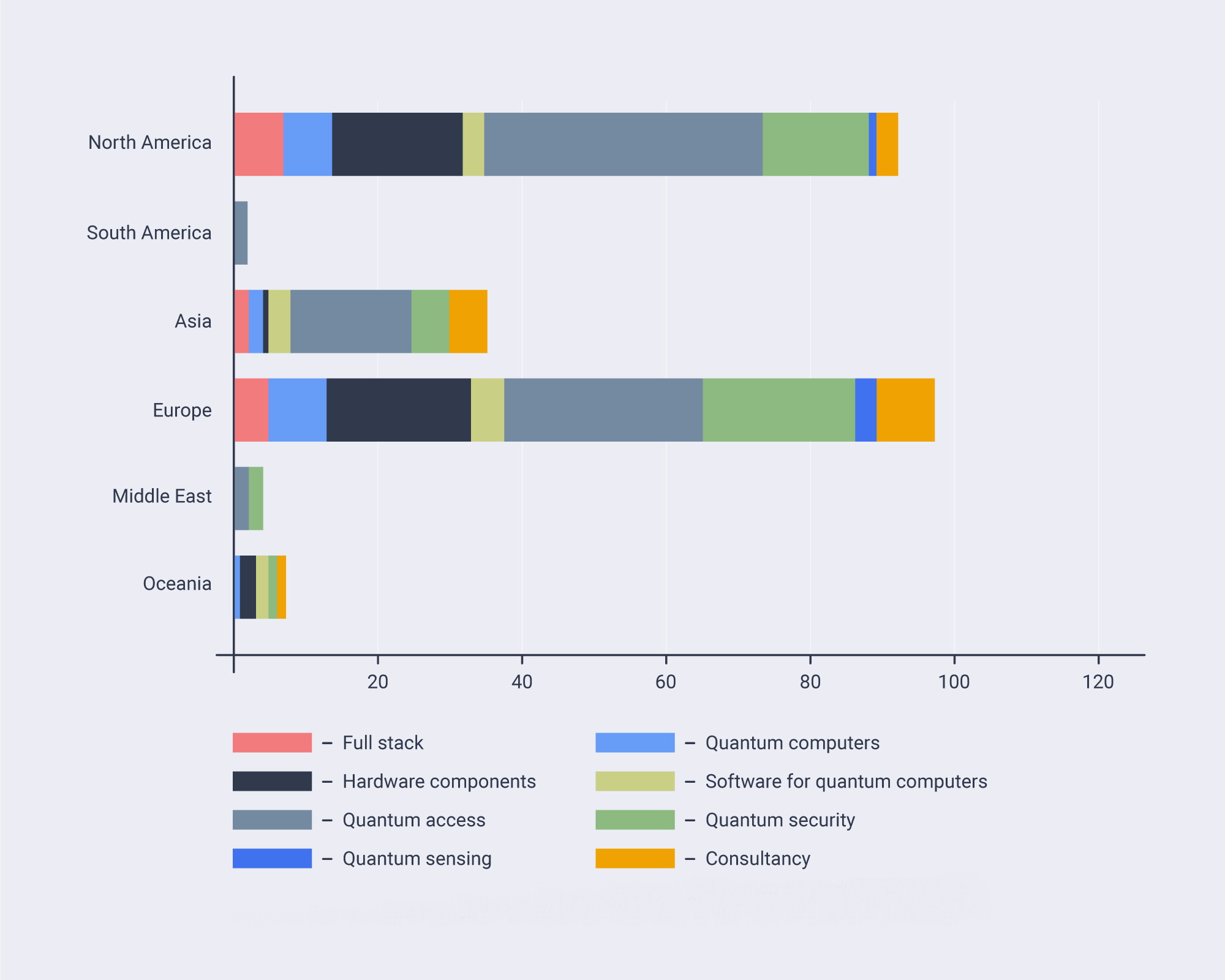

The database analyzed contains 239 companies that offer services related to quantum technology. Europe (including the UK) and North America are relatively similar in terms of the number of companies and type of services provided. Approximately 30 percent of the companies in Europe operate in the UK.

Unlike North American companies that focus on facilitating access to quantum computers and developing applications for quantum technologies, European companies seem to be more evenly distributed in terms of activity, with a relatively similar number of businesses producing quantum hardware components, facilitating quantum access, and providing quantum security solutions. Nevertheless, quantum access is the most strongly represented sector in this industry in all regions except for Australia (Oceania), which chooses to concentrate its efforts on developing hardware components and software to improve quantum computers’ accuracy.

No efforts to build quantum computers have been registered in Middle East, where the focus is solely on envisioning applications for quantum computers and developing quantum-safe encryption.

In Asia, public and private companies are mainly engaged in the quantum access sector (49 percent of companies), followed by developing secure quantum communication, consultancy, and software development. The two Chinese giants Alibaba and Baidu are developing their own quantum computers and provide access to them via cloud

Besides companies offering products and services related to quantum technologies, a significant number of umbrella organizations have emerged, mostly supported by governmental funds.

In the US, the Quantum Economic Development Consortium (QEDC) brings together the main stakeholders in the quantum industry (135 corporations, 32 academic institutions, 6 national labs, and 7 professional societies) to assess the current research needs and advance the development of this field.

In the UK, established businesses, startups, research centers, and universities have teamed up in the Discovery Project (considered the largest industry-led quantum computing project in the UK to date)89 to tackle the challenges related to quantum computing.

In Europe, there are multiple organizations at the national level such as the Bavarian Quantum Computing eXchange (aims to find ways to combine and harness the power of both quantum and supercomputers), the French Alternative Energies and Atomic Energy Commission (CEA), the Swiss Quantum Hub, the Spanish National Research Council, etc.

The Quantum Flagship – a project initiated by the European Commission – aims to involve over 5,000 researchers over a period of more than ten years to harness the potential of quantum computers and develop a quantum web.

In Asia, the Quantum Technology Foundation Thailand is building a strong community of scholars and business representatives to promote “quantum thinking” and increase the industry’s adoption of quantum technologies.

In the Middle East, Iran’s Quantum Technology Center promotes the efforts of local players to speed up the developments in the field of quantum computing, quantum sensing, communication, and simulation.

At the global level, the Quantum World Association closely follows the developments in the field, connects scientists and companies, and provides field expertise.

Main universities and research centers

Main universities and research centers

Universities have been at the forefront of quantum technology development, with research centers scattered across the globe, mostly within physics departments. Once the research results were incorporated into business projects and started to spread to various industries, developments in the field accelerated, and an increasing number of educational institutions started to initiate quantum research projects, either as stand-alone divisions or adjacent to other already existing departments.

The number of universities offering research opportunities related to quantum technology is constantly increasing. However, most of them only have research groups related to quantum computing, and just a handful offer postgraduate-level courses or have incorporated the topic into their curricula.

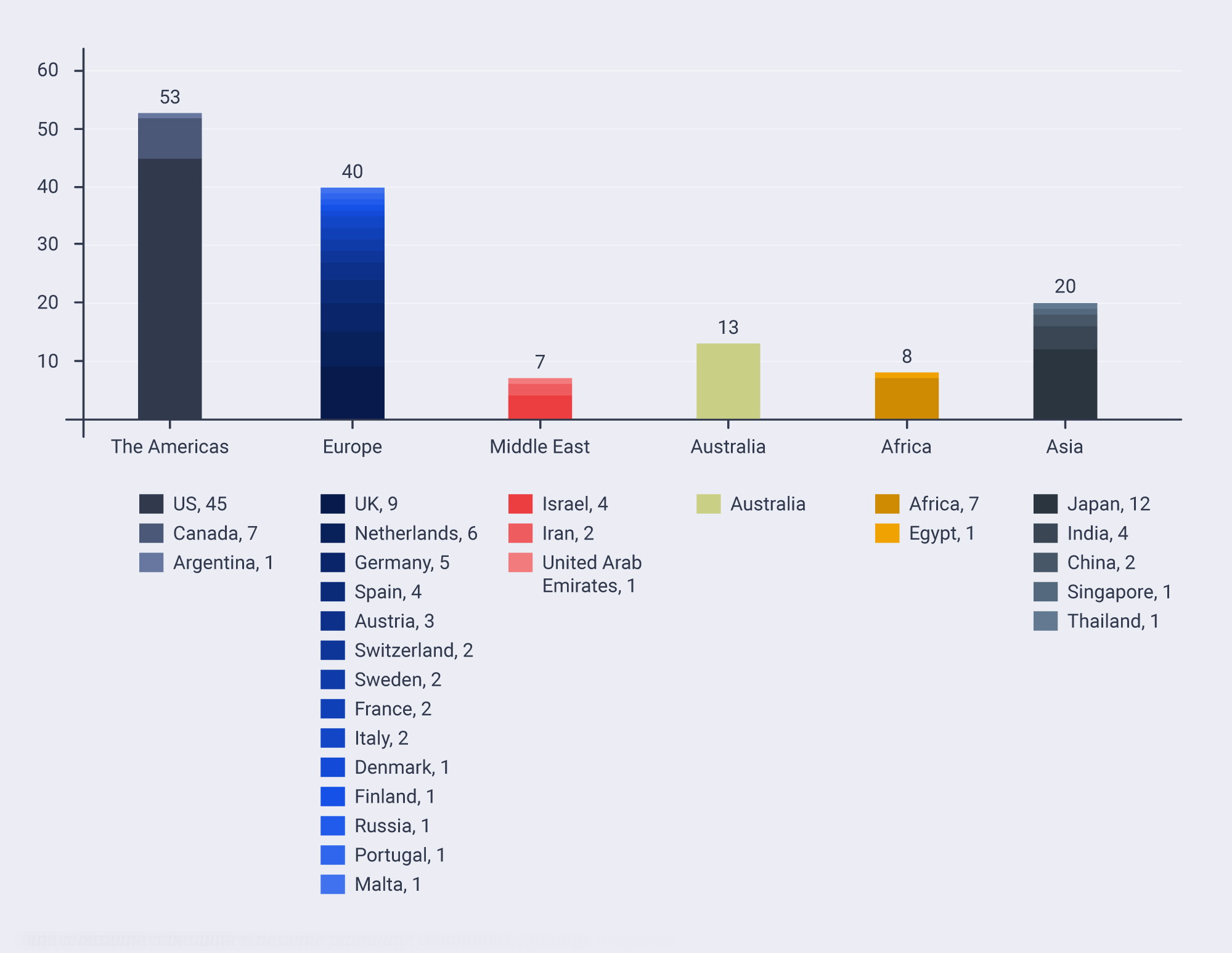

The US leads the way in terms of both reputation and the number of universities with quantum computing related programs.

With its Joint Quantum Institute, the University of Maryland is considered one of the top universities in the world that have research programs dedicated to quantum computing. With over 200 researchers in this field, it ranks among the institutions with the highest concentration of quantum specialists. A part of the technology developed in the university’s labs was licensed to IonQ, a promising start-up co-founded by Professor Chris Monroe that aims to build the fault-tolerant quantum computers of the future.90

Other notable universities are the MIT Lincoln Laboratory with its projects on quantum information and integrated nanosystems, the California Institute of Technology’s Institute for Quantum Information and Matter (IQIM), the Harvard Quantum Initiative (HQI), and the Center for Quantum Information and Control (CQuIC) at the University of New Mexico.

With nine universities which have programs dedicated to the study of quantum technologies, Canada established itself as one of the leaders in this area

For a long time, Waterloo’s Perimeter Institute for Theoretical Physics was at the forefront of developments in quantum technologies, and the Institute for Quantum Computing within the University of Waterloo has raised expectations. According to research conducted between 2007 and 2016, this university ranks second in terms of the number of papers published on this topic.91

All European countries taken together have the second-largest number of research institutes after the US.

Université Grenoble Alpes is highly active in this field, with numerous industry partners. Along with Université Paris-Saclay, Grenoble is considered one of the most advanced sites for the development of France’s strategy around quantum technologies.

The University of Oxford is the leader in terms of the number of scientific papers published in the field of quantum computing, with 38 research teams and over 200 researchers. It focuses mostly on quantum optics, low-temperature superconducting devices, and quantum materials as well as theoretical and experimental studies.

Other universities with notable research results and partnerships with the industry are Delft University of Technology, the Netherlands Organisation for Applied Scientific Research (TNO), LMU Munich and its Quantum Applications and Research Laboratory (QAR-Lab), the Quantum Information & Computation research group at the University of Innsbruck, and ETH Zurich.

Despite having less research centers than Europe and America, Asia stands out through its achievements and high level of governmental support.

The National University of Singapore hosts the Centre for Quantum Technologies with over 150 scientists and researchers, focusing on quantum theory, computation, and simulation.

Australia has six universities offering quantum computing programs or research centers.

An important node in the Microsoft Station Q network is the University of Sidney, which conducts research in the quantum field through its Quantum Science Group. The activities range from theoretical research to technology development and experimental research focused on semiconducting qubits and trapped ions.

While quantum research in Africa is only getting started, various institutes on the continent are planning to steadily increase their involvement in quantum computing.

Besides IBM’s center in Johannesburg, South Africa’s University of KwaZulu-Natal is doing research in the field of quantum computing for more than a decade, while in 2018 the University of the Witwatersrand also joined the IBM’s Quantum Computing Network. Theoretical research and experiments have been done both in the field of quantum computing as well as quantum communication. Even though interest on the part of the industry still seems to be low, academics hope that things will change with more governmental spending and the development of educational programs at university level in this area.

Patents

Patents

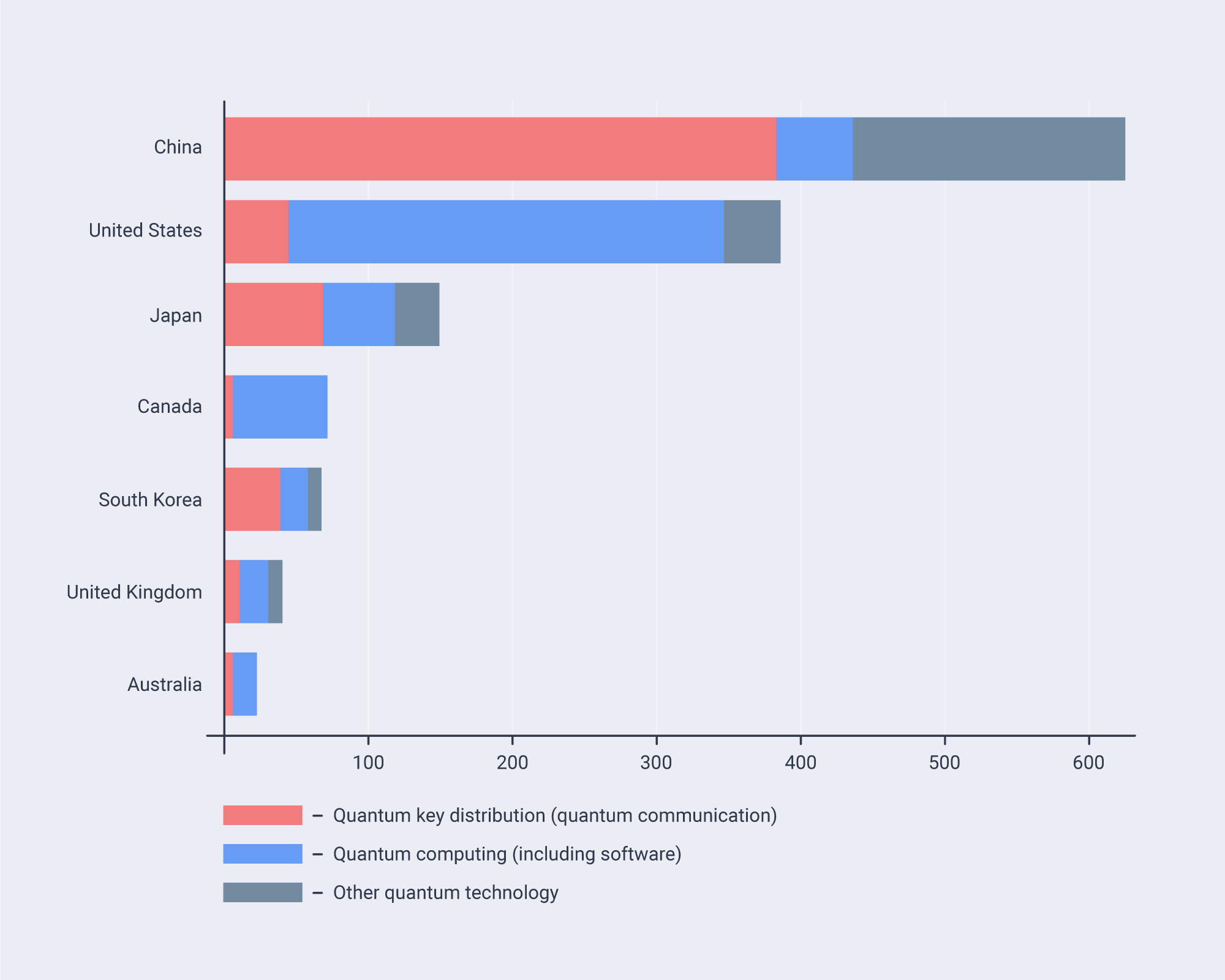

In terms of patents, China is at the forefront of the industry, with over 600 patents registered since 2012. An analysis conducted by EC Joint Research Institute shows the US in second place, followed by Japan, Canada, and South Korea.92 Asian researchers seem to be more focused on quantum key distribution and quantum security, while actors in the US, Canada, the UK, and Australia are focusing more on quantum computing and software applications.

Despite the growing number of research institutions and university centers active in the field of quantum computing, there is still a shortage of specialists. However, the number of universities introducing quantum technology in their curricula is constantly increasing.

References

[86] Petar Jurcevic et al., “Demonstration of Quantum Volume 64 on a Superconducting Quantum Computing System,” ArXiv:2008.08571 [Quant-Ph], September 4, 2020, http://arxiv.org/abs/2008.08571.

[87] “IBM’s Roadmap For Scaling Quantum Technology,” IBM Research Blog (blog), September 15, 2020, https://www.ibm.com/blogs/research/2020/09/ibm-quantum-roadmap/.

[88] “Quantum Computing Startup Raises $215 Million for Faster Device,” Bloomberg.Com, April 6, 2020, https://www.bloomberg.com/news/articles/2020-04-06/quantum-computing-startup-raises-215-million-for-faster-device.

[89] Matt Swayne, “UK Quantum Firms Team Up For DISCOVERY, a £10 Million Research Program,” The Quantum Daily, November 8, 2020, https://thequantumdaily.com/2020/11/08/uk-quantum-firms-team-up-for-discovery-a-10-million-research-program/.

[90] Maryland Today, “UMD Ranked Among World’s Top Quantum Computing Research Universities,” The University of Maryland Today, November 22, 2019, https://today.umd.edu/briefs/umd-ranked-among-worlds-top-quantum-computing-research-universities-bf7edbc8-1558-41f1-9f0e-aed246dec907.

[91] S. Dhawan, Brij Mohan Gupta, and Sudhanshu Bhusan, “Global Publications Output in Quantum Computing Research: A Scientometric Assessment during 2007-16,” Emerging Science Journal 2 (September 11, 2018), https://doi.org/10.28991/esj-2018-01147.

[92] Elizabeth Gibney, “Quantum Gold Rush: The Private Funding Pouring into Quantum Start-Ups,” Nature 574, no. 7776 (October 2, 2019): 22–24, https://doi.org/10.1038/d41586-019-02935-4.