Consequences for established sectors

Consequences for established sectors

Initially, cultured meat will be a novelty, with little impact to be expected for the global meat trade. Though the cost of in-vitro meat has gone down considerably since Mosa Meat presented the first lab-grown burger patty, it is not competitive today in terms of price.

According to Supertrends expert Erdem Erikçi, the critical elements are the cost of components such as scaffolds and bioreactors, efficient growth medium use, and the availability of a cheaper alternative to fetal bovine serum. He believes in-vitro meat will not appear on a restaurant menu before 2024. Even then, it is likely to be a niche product that is not widely available.

Nevertheless, assuming that cultured meat can be scaled up and that the technology achieves market maturity as well as regulatory approval and acceptance by consumers, it would mark a watershed for the traditional meat industry. Obviously, the degree to which cultivated meat will disrupt their business would largely depend on the speed of transition, but also on how it responds. In reality, the response by the traditional food industry to the prospect of competition from cell-based meat has been twofold. Some industry bodies and trade associations have initiated efforts to push back against the emerging technology. These lobbying drives (which are directed not only against cellular agriculture, but also against other plant-based meat analogues) focus on issues related to labeling and consumer protection.

However, some of the leading meat corporations are taking the opposite approach, embracing cultured meat and seeking to establish themselves as market players while the business is still in the embryonic stage. And in the EU, regulatory efforts may prove favorable to in-vitro meat, which could help governments achieve their stated goals in connection with climate change mitigation, food security, and promotion of innovation. Indeed, some of the biggest names in the food industry have entered into partnerships with startup companies in the cultivated meat business, possibly prompted at least in part by the successful introduction of meatless burgers in a number of restaurant chains. For instance, fast-food conglomerates such as McDonald’s, Burger King, Carl’s Jr., and Tim Hortons have added plant-based patties made by producers such as Beyond Meat and Impossible Foods to their menus, proving that consumers are willing to accept alternatives to meat from butchered animals.

As another example, Dutch cultured meat pioneer Mosa Meat, has received funding from the Bell Food Group, the leading meat-processing company in Switzerland, whose majority shareholder Coop is one of the top national retail and wholesale companies and sells half of the country’s organic food produce. Among the other investors in Mosa Meat are Google co-founder Sergey Brin; Nutreco, a Dutch manufacturer of processed meat products as well as animal nutrition and fish feed; and EMD Group, a subsidiary of German bioscience company Merck. Similarly, Israeli in-vitro meat startup Future Meat Technologies has attracted investment from Tyson Ventures, the venture capital arm of Tyson Foods Ltd. As the largest US meat producer with annual revenues of US$40 billion (2018), and the second-largest in the world, Tyson Foods is clearly the kind of industry heavyweight that can expedite the mass commercialization of cultured meat. The funding raised by Mosa Meat (€7.5 million) and Future Meat (US$16.2 million) pales in comparison to the US$161 million founding round announced by San-Francisco-based Memphis Meats in January 2020. Among its backers are not only food giants such as Tyson Foods and the Cargill conglomerate (the largest privately held US corporation by revenue), but also prominent individual investors and venture capitalists such as Bill Gates, Richard Branson, and Kimbal Musk (Elon Musk’s brother). Other investors in the space include Draper Fisher Jurvetson (DFJ), Khosla Ventures, Kleiner Perkins, and similar top names in the venture capital industry. The involvement of these industry players has done much to raise the profile of the cell-based meat industry as a whole and to underscore the technology’s fundamental viability.

New business models for the meat industry?

These changes may happen quickly or slowly, but in either scenario, the meat industry would have to make significant adjustments. A potential opportunity for those enterprises willing to change their business models would be to switch from manufacturing and food production to a service-based concept. Instead of raising and butchering live animals, they could manufacture and supply components for bioreactors, and provide operation and maintenance services for the hardware elements of the cultivated meat infrastructure; provide the myosatellite stem cells that are needed to cultivate muscle tissue; develop improved scaffolds for structured meat cuts; and supply growth media or manufacture nutrient solutions for the growth of cell cultures. Supertrends expert Robert ter Hoor has pointed out that once there is an installed base of cultured meat machinery, vendors would be able to expand their business by selling growth hormones, medium, etc.

Incidentally, Future Meat has described an interesting business model. While some cultured producers are committed to producing the meat themselves or, for example, in collaboration with pharmaceutical companies that are good at operating bioreactors, Future Meat has developed a kit for farmers. The farmers then have to buy everything they need to produce cultured meat, including both mechanical equipment and raw materials. Once the meat has been grown, it is delivered back to Future Meat Technologies for processing, so that they can achieve optimum taste and texture. Even if animal husbandry and meat production on an industrial scale are displaced by in-vitro meat technology, there may still be a niche market for meat from animals raised on small family farms. Indeed, the arrival of cultured meat could help ensure the survival of such smaller-scale agricultural enterprises as “real” animal meat from local producers would be marketed to wealthy consumers as a rare luxury good. This could also be combined with eco-tourism.

In accordance with the UN Sustainable Development Goals, traditional agriculture industries are already undergoing a transition towards more sustainable operations that are less harmful to the environment and the global climate, and more in line with the needs of workers in the sector. A 2018 report by the International Labour Organization found that while vegetable, fruit, and nut farming will see the strongest decline in job demand due to this shift, the meat industry can expect the highest growth, with new jobs being added in poultry farming (600,000), pig farming (500,000), cattle farming (500,000), and cultivation of other meat animals (100,000) due to the transition to sustainability in agriculture [79].

However, this picture would obviously change given a widespread adoption of cell-based meat, which would pose a fundamental challenge to livestock breeders. With the ability to cultivate tens of thousands of tonnes of meat from just a few stem cells in bioreactors, the need to maintain large herds of animals, which require a great deal of effort and expenditures to raise and tend, would be eliminated or sharply reduced. The impact would be especially drastic in those national economies that supply most of the world’s meat, including the top beef-exporting countries (Brazil, India, Australia, US, and New Zealand). Exporting meat in very large quantities would eventually become less viable as countries that are now net importers might produce more by themselves and even become fully self-sufficient, covering their needs with cultured beef, pork, mutton, and chicken. As of 2016, the main meat-importing regions and countries were Sub-Saharan Africa, Saudi Arabia, Indonesia, the Philippines, and Vietnam [80].

Owners of grazing land

Which commercial value could landowners derive from agrarian estates if incomes from grazing rights and leaseholds were to disappear? While some cattle ranchers might be able to switch to dairy farming or crops (with potential further knock-on effects for those sectors arising from new market entrants and surplus capacities), this will not be an option for the entire industry. A major reduction or virtual disappearance of traditional animal husbandry – whether rapid or gradual – would not only impact farmers, but also have further-reaching ramifications for the entire meat industry and associated sectors, such as rural banks and more.

Tractor and equipment manufacturers

Eventually, once the adaptation of cultured meat eventually makes a real impact on the traditional farm industry, the demand for tractors and other farming equipment will drop. As a result, an oversupply of used equipment will translate into a very sharp drop in demand for new equipment. Even worse, as the values of used equipment drops, equipment lease payments will go up to compensate for decreased residual values, which will push prospective buyers further towards the used equipment market. This vicious cycle can then lead to bankruptcies, higher financing costs, and decreased economies of scale in the equipment manufacturing sector, which will even worsen the vicious cycles.

The fact that cell-based meat comes from a bioreactor rather than from an animal means that it can be manufactured wherever the device is installed, independently of environment, geography, or climate. For suppliers of conventional produce, it would entail considerable reconfigurations and changes all along the supply chain. As noted above, dislocation and decentralization of the meat industry could strongly affect the countries where – at least in certain regions – external conditions have traditionally favored livestock farming, and whose GDP relies heavily on the meat industry. However, such a restructuring would also have implications for meat processing, packaging, distribution channels, logistics, freight, storage, and retail around the globe.

A changing urban landscape

Far-reaching restructuring and shifts in the meat industry’s supply chains could be reflected in urban development. Slaughterhouses and meatpacking plants used to be located within city limits. They were frequently unregulated and constituted health hazards to workers and the general public (the term “shambles” originally referred to open-air slaughterhouses and the chaotic conditions that prevailed there).

As populations became increasingly urbanized, and as the hygienic problems associated with high population density became more apparent and better understood, abattoirs were moved to designated industrial zones on the outskirts of the city. Gradually, economic globalization combined with new refrigeration technologies and expanded transport capacities made it possible to deliver frozen meat across long distances. “Locally sourced” meat, previously the only option, became a niche product competing with cheaper overseas imports. With the ability to produce cultured meat in compact plants under sterile conditions, this could change. Suppliers could once again operate locally inside urban areas, in close proximity to consumers. They would be able to tailor their production quite precisely to demand, and with much shorter distribution channels, giving them a competitive edge over suppliers of conventional meat.

Reconfiguring the supply chain

Conversely, widespread adoption of in-vitro meat could significantly reduce the demand for long-range shipping and freight capacities for frozen meat, as well as animal feed. Eliminating the need for feed haulage would have a particular impact in the US and other countries where cattle are fattened on grains such as soy and corn rather than grass.

Independent butcher’s shops and charcuteries, already in steady decline due to competition from supermarkets, would probably come under even greater pressure due to competition from cell-based meat. Conversely, some analysts argue that, as traditional meat becomes a cheaper option, these independent outlets could benefit and carve out a niche as suppliers of “real” meat as a luxury product.

Packaging, retail, byproducts

Other sectors in the supply chain might be less affected by the market entry of cultured meat. Both raw and processed meat – whether cultivated meat or traditional – must be packaged for reasons of hygiene, to extend shelf life, and in order to preserve appearance and palatability, among other properties [81]. If, as seems likely, cultured meat would initially be available mainly in the form of ground meat, burger patties and the likes, the current standard packaging for those products would presumably be used.

In the first stage of commercialization, the in-vitro meat industry would obviously not be able to offer anything like the full range of structured meat cuts and products that are currently available from traditional producers, which require a broad variety of packaging solutions, ranging from plastics and polymers to glass containers, aluminum tubes, and natural casings [81]. At the final stage of the supply chain, retailers would probably also see comparative few changes, at least initially. From a logistical standpoint, it would make little difference to a vendor whether the meat products that are stocked and sold are derived from traditional meat production or through cellular cultivation.

Some observers speculate that in the long term, retailers could eventually be removed from the equation as bioreactors become available for home use. However, given the complexity of the technology and issues surrounding hygiene and food safety, it is very unlikely that private households will want to, or be able to, cultivate their own meat in a bioreactor for decades to come, if ever. Moreover, it is questionable whether consumers would want that. Indeed, some Supertrends experts have indicated they do not believe bioreactors for home use will be widely available for many years to come.

Looking beyond the core business of the meat industry, there are other byproducts of livestock farming that are economically significant, such as leather, wool, fertilizer, chemicals, or rendered fats. A substantial reduction of animal herds or flocks would lead to supply shortages of these goods, leading to steep increases in prices both of the raw materials and the products made from them, such as leather goods. They might have to be sourced through other means, or be replaced with synthetic or alternative products, while the “genuine” materials would become luxury items.

The US company Modern Meadow is working on a biofabricated leather product under the brand name “Zoa”. Instead of the cell cultivation harnessed for cell-based meat, yeast cells are used that have been genetically engineered to produce a fibrous material from collagen, a protein normally found in cow hide, which is treated in the same way as normal leather. Due to the production process, the material can be made stronger and lighter than traditional leather. Artificial leather may thus be different from the natural kind. Although it feels like real leather, its properties may be more closely tailored to consumers' needs. It may be produced in a more environmentally-friendly manner and devoid of ethical dilemmas associated with animal welfare.

Obviously, if “clean meat” were to replace traditional produce, the effects would be felt most acutely at the first stage of the value chain, by the butchers and slaughterers working in abattoirs. If cultured meat replaces traditional farming, meatworkers in slaughterhouses and renderers will lose their jobs. Renderers are companies that do recycling of slaughter byproducts for the livestock industry. More than 90 percent of their raw material is cycled back to the farm business where it is used as animal feed. However, as more and more products that traditionally come from cattle can be made synthetically, more and more renderers will see their businesses erode.

However, it should be mentioned in this context that jobs at slaughterhouses and renderers are not considered very attractive compared to many other industries. Indeed, it has been shown that farmers and meatworkers experience psychological damage from the constant exposure to violence and the institutional climate that prevails on killing floors, resulting in higher propensity for violence and crime in communities centered on meat processing facilities [82];[83].

These are mostly physically demanding unskilled jobs. According to the US Bureau of Labor Statistics, 135,500 workers were employed in the US as butchers in 2018, with a median pay of US$31,580 per annum. In the EU, as of 2011, there were 124,600 enterprises specializing in meat products with 358,000 employees. It is uncertain how many employees from the traditional industries can be re-skilled for work in the in-vitro meat chain, which would include large-scale production of growth media [84]. While the loss of some of these jobs would obviously be difficult for many of the workers in question and their communities, it might in fact be helpful to the meat industry as a whole. The elimination of abattoirs could not only lead to a significant improvement of meat quality and working conditions but could enhance the industry’s overall image and stimulate demand as a result.

Impact on fishery and seafood harvesting

Impact on fishery and seafood harvesting

Most of the impacts listed in the previous sections would also apply analogously to the fishing industry. Widespread adoption of fish meat manufactured in vitro from stem cells would threaten jobs and disrupt supply chains built up over centuries. At the same time, maritime pollution has gained more and more attention in recent years, so the ability to produce seafood that is free from microplastics and contamination with mercury and other heavy metals would be welcomed by consumers. Unlike the meat of fish and crustaceans, which is highly susceptible to spoilage and requires sophisticated logistics, cultured seafood could be manufactured anywhere on the planet and consumed close to its point of origin.

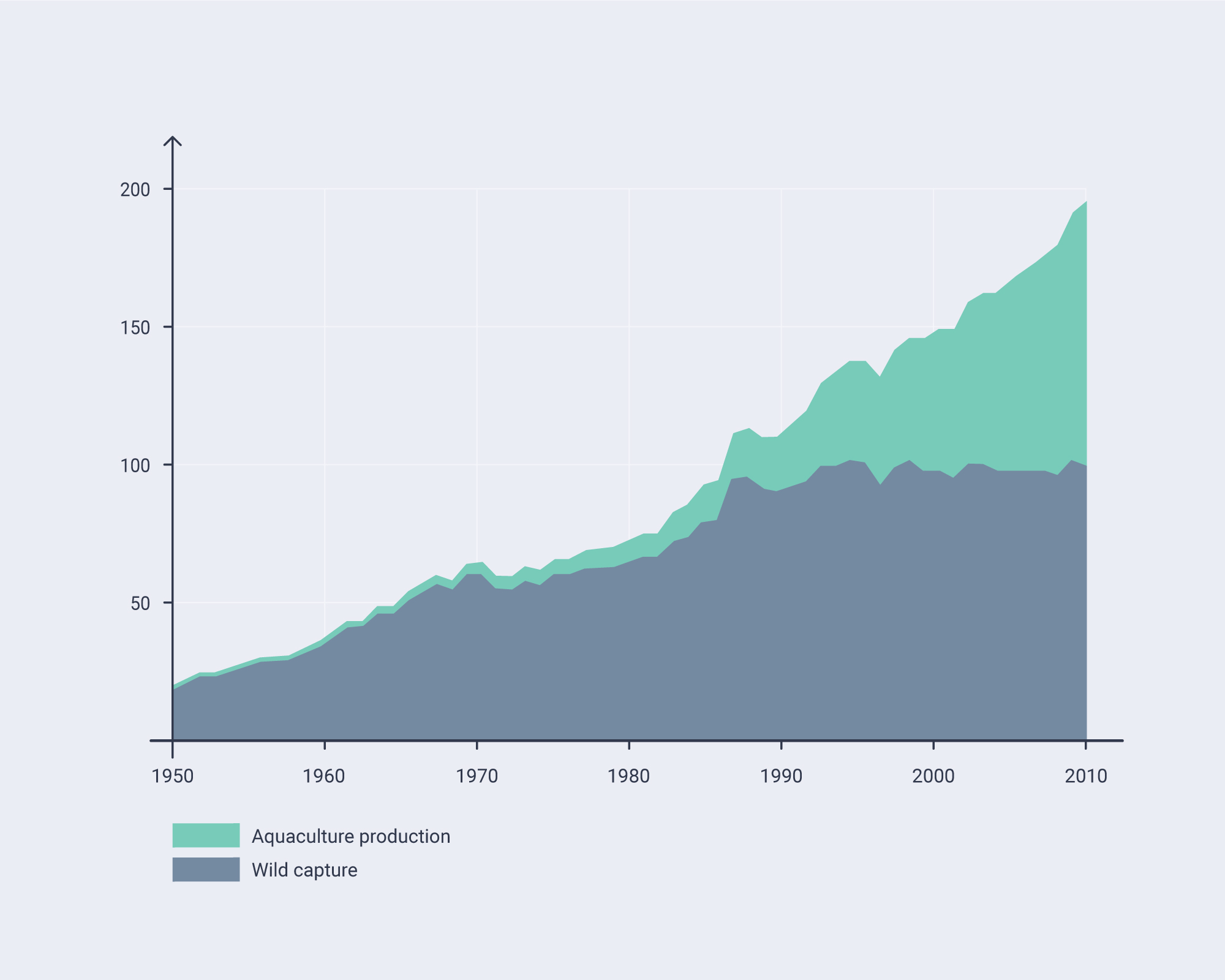

What sets the fishing industry apart from livestock farming on land is the fact that fish are not “domesticated” in the same sense as cattle, pigs, or sheep. According to the FAO’s Fisheries and Aquaculture Information and Statistics Branch, aquaculture (farming of seafood organisms under controlled conditions) accounted for nearly 112 million tonnes of produce with a value of about US$250 billion in 2017, the last year for which data was available. This was equivalent to just over half of total global seafood production (205.5 million tonnes).

Relieving pressure on fish stocks

However, this means a significant share of seafood consumption is still supplied by maritime fishery fleets, essentially a form of hunting that has increasingly been diminishing the world’s stocks in recent decades. This is a problem that has no comparable analog in the land-based meat industry, and one that could be alleviated through cultured fish meat.

Generally speaking, it appears likely that seafood producers engaging in aquafarming will be better able to remain competitive with cultured seafood, while the traditional fishery industry – already under pressure from aquafarmers and environmental activists alike – might find it difficult to defend their market shares. As with meat, however, it will probably take a while for traditional methods to be fully displaced, and by complementing the existing range of produce, cultured fish could relieve pressure on natural resources and thus even extend the viability of the world’s fishing fleets beyond what currently appears likely.

Regulatory frameworks

Regulatory frameworks

As discussed above, regulatory approval will be key in determining the viability of cultured meat technology. Health and safety considerations will be paramount, but overarching policy goals will also factor into the equation. In the EU, where agriculture and food production account for 4.4 percent of overall GDP and 8.3 percent of employment [85], competition from synthetic meat would also be likely to have a far-reaching disruptive impact, especially in underdeveloped and remote regions with predominantly agrarian economies. Approval of in-vitro production would depend on compliance with the EU’s regulations regarding genetically modified organisms, which are considered the strictest in the world [86], and the use of hormones in food production.

Cultured meat as a lever for policy goals

However, consumer protection is not the only factor that Brussels must take into consideration. Cell-based meat could prove a welcome addition to the EU’s toolbox in achieving ambitious targets for climate protection and food security. The European Commission (EC) plans to reduce GHG emissions by at least 40 per cent compared to 1990 levels by the year 2030. Even a partial switch from livestock breeding to cellular agriculture could help to make those targets achievable. In the sphere of food security and sustainability, one of the EC’s goals is to increase the consumption of healthy and sustainable diets by doubling the diversity of accessible energy and protein food sources. An independent expert report commissioned by the EC specifically listed in-vitro meat among “protein sources suitable for human consumption with relevant nutritional profile and sustainability footprints that are not produced or processed in sufficient amounts” [87].

In June 2019, responding to a question submitted in the European Parliament, then EU Commissioner for Health and Food Safety Vytenis Andriukaitis noted that this expert report had identified “new meat alternatives as an important pathway to achieving the Commission’s Food 2030 Initiative, to deliver a climate-smart and sustainable food system for a healthy Europe”, while pointing out that pursuant to Regulation (EU) No 2015/2283(2) on novel foods, cultured meat would require pre-market authorization as well as being subject to “the general principles and requirements of food law in terms of e.g. responsibilities of the food business operators and traceability of the food, and to the provisions on food information to consumers in order to provide a basis for final consumers to make informed choices.”

Takeaways

Takeaways

The displacement of traditional meat and fish by cell-based meat products will not take place overnight, but even a gradual shift would create very significant disruption in the global meat industry, with repercussions in associated sectors as well. Almost all stages of the supply chain would be affected to varying degrees.

A decentralization of meat production would hit meat-exporting countries hard, directly affecting GDP and employment, but would help net importers become self-sufficient.

While some trade associations are lobbying to stem off the competition from cultured meat and other meat analogues, other players are already moving to secure a stake in the nascent cellular agriculture sector, as underscored by a rapidly growing influx of venture capital.

Regulators, who will have a key role in determining the viability of cultivated meat, will not only have to consider health and safety questions, but also take into account the potential contribution of the new technology to achieving essential national, regional, and global policy goals.

[79] “World Employment and Social Outlook – Trends 2018” n.d., 82:50.

[80] OECD-FAO 2016. Agricultural Outlook 2016-2025

[81] Kurrer, C. and C. Lawrie 2018. What if all our meat were grown in a lab? European Parliamentary Research Service, Scientific Foresight Unit (STOA). http://www.europarl.europa.eu/RegData/etudes/ATAG/2018/614538/EPRS_ATA(2018)614538_EN.pdf. Accessed: 24 April 2020.

[82] Richards, E. et al. 2013. A Different Cut? Comparing Attitudes toward Animals and Propensity for Aggression within Two Primary Industry Cohorts — Farmers and Meatworkers. Society & Animals 21:395–413.

[83] McMillin, K.W. 2017. Advancements in meat packaging. Meat Science 132:153-62

[84] Mattick, C. et al. 2015. A case for systemic environmental analysis of cultured meat. ScienceDirect 14(2): 249-254

[85] Davison, J. 2010. GM plants: Science, politics and EC regulations. Plant Science 178(2):94–8. doi:10.1016/j.plantsci.2009.12.005

[86] European Commission, Directorate-General for Research and Innovation 2018. Recipe for change: An agenda for a climate-smart and sustainable food system for a healthy Europe.

[87] UNDP 2019. SDG Localization in ASEAN: Experiences in Shaping Policy and Implementation Pathways.